*Note: a SWOT analysis is an evaluation of the fundamental, operational, technical, social, economic, and even to some degree administrative elements of a project. This is not a model to be used for trading purposes. (NFA, DYOR)

Composed of four elements, Strengths, Weaknesses, Opportunities, and Threats, a SWOT analysis framework provides excellent insight for establishing a high-level understanding of the state of a project's well-being through the lens of a birds-eye view.

It can help formulate decisions around which areas require more attention, set performance goals, and organize a foundational understanding of where a project is headed.

Rarely (if ever) used in crypto, it is time to apply this timeless method of evaluation to the digital asset space.

Today, Moonbeam (GLMR), the leading EVM-compatible smart contract platform built on Polkadot, will get a SWOT.

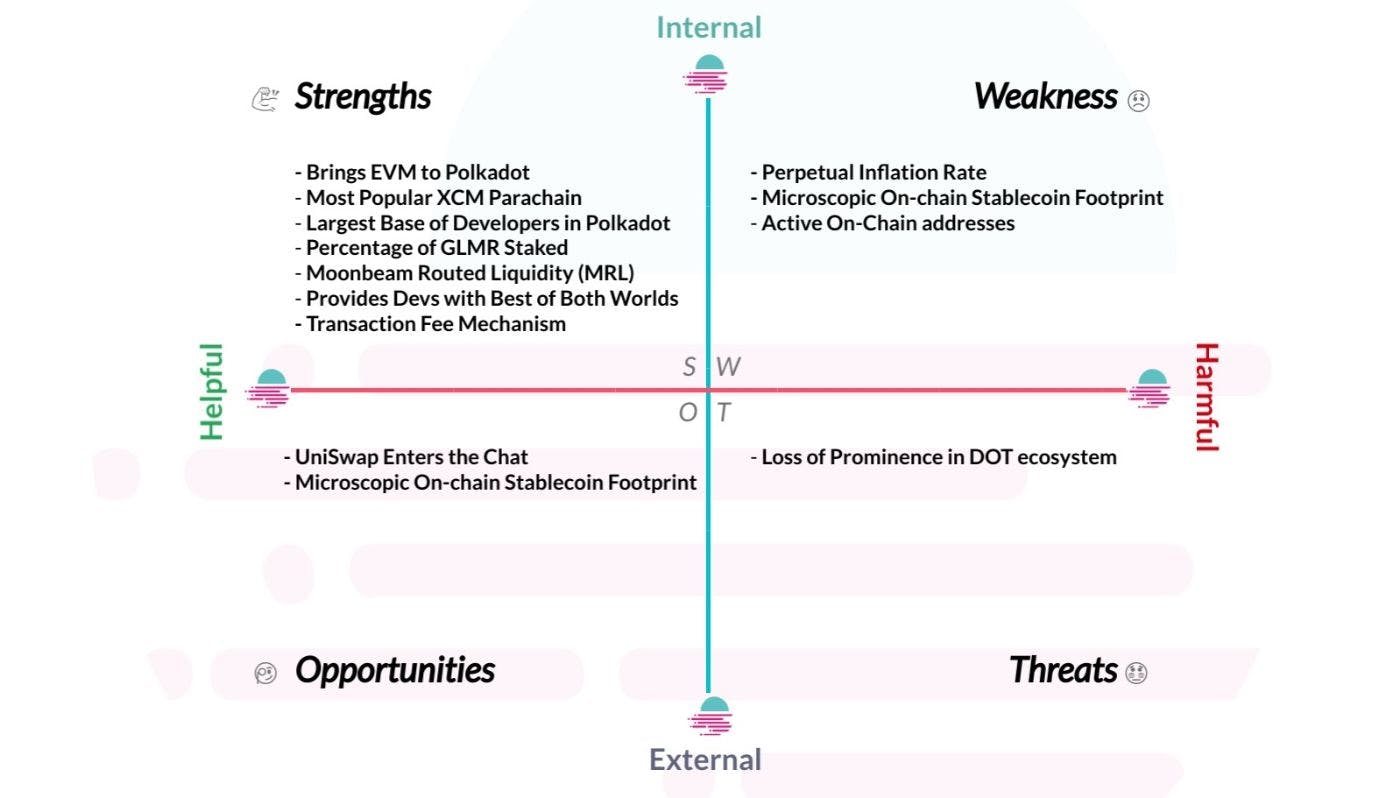

💪 Strengths (Internal) (Helpful)

1. Brings EVM to Polkadot

The EVM has become the de facto environment in the blockchain space with the most robust smart contract tooling, developer mindshare, and operational applications. Polkadot's grand mission of interoperability and scalability is hindered by the fact that the current industry standards have aggregated around the Ethereum ecosystem. By extending the EVM's capabilities to Polkadot, novel hybrid chain solutions can be designed that are not limited to either environment, and the benefits of both can be synthesized into something where the whole is greater than the sum of the parts.

2. Most Popular XCM Parachain

XCM is Polkadot's Cross-Chain-Messaging protocol that allows parachains the capability to transfer data between networks. Moonbeam's XCM channel with Acala network is the most utilized of all Polkadot network XCM channels. Leading in this metric indicates that moving forward, more likely than not, all of the other parachains will, in some way, shape, or form, establish channels with Moonbeam as well. In fact, many of the leading projects, such as Origin Trail, Centrifuge, and Nodle, already have.

3. Largest Base of Developers in Polkadot

The greater Polkadot/substrate ecosystem proudly places 2nd (right behind Ethereum) for the number of developers in the space. Out of all the projects being built, Moonbeam has the most of all. Of the 621 full-time devs, approximately 200 are working on Moonbeam. Considering that there are 48 parachains live on mainnet, and Moonbeam alone has 1/3 of all the developers, the pure intellectual dominance positions Moonbeam as a leader with no competition breathing down their neck.

4. Percentage of GLMR Staked

The ratio of the circulating token supply that is committed to the network has been steadily growing. Over the course of the last year, the amount of GLMR staked has grown every quarter, rising from 16.5% to 24.7% to 28% to 32.2% to 36.4%. The growing percentage of tokens staked signals holder confidence and exerts positive forces on the token's price over the longer term. As more of the supply gets locked, the liquidity tightens, creating more sensitive price action and providing a higher degree of confidence around the potential selling pressure.

5. Moonbeam Routed Liquidity (MRL)

Liquidity is the pinnacle of financial parameters in crypto. Notorious for its extremely high levels of fragmentation (especially after the introduction of the modular/interoperability frameworks), blockchains have created a catch-22 whereby new networks are unable to attract the liquidity that has been captured by applications on other networks. Moonbeam leveraged Polkadots XCM capabilities to build a liquidity router that plugs into the Wormhole bridge via HydraDX and allows Substrate protocols to tap into liquidity on other networks such as Solana, Ethereum, and Avalanche. MRL effectively supercharges Moonbeam with the power to help previously non-interoperable environments share data and information in a fluid manner.

6. Provides Developers with the Best of Both Worlds

By design, Moonbeam inherits desirable properties for developers from both its Ethereum WEb3 RPC API and Substrate RPC, allowing developers the flexibility to interact with Moonbeam nodes through whichever suite of tools they prefer. Being developer-friendly is the lynchpin that fundamentally sets apart projects that will continue to have flourishing ecosystems and those that will be disregarded.

7. Transaction Fee Mechanism

While it is commonplace for large smart contract networks to distribute (at least some) of the TX fees among network node operators, Moonbeam has opted to modify this by distributing them into two baskets, having 80% of the fees being burned (to create countervailing deflationary forces that combat the emissions) and 20% deposited into an on-chain treasury that is utilized as deemed necessary by the governance forum. It seems that this mechanism would, at least in theory, create a harmonious balance that invites participation from governance while damping the effects of economic devaluation over the long term.

😞 Weaknesses (Internal) (Harmful)

1. Perpetual Inflation Rate

Inflation is the silent thief of economic opportunity from the average market participant. Standing at 5% per year, GLMR has a programmatic supply increase that dampens its impact over the course of time. It should be noted that how these newly minted tokens are injected into circulation plays a vital role, and here Moonbeam did a decent job in diffusing the potential negative price impact by splitting them into 3 incentive categories: 1% to collators (block producers), 2.5% to stakers, and 1.5% to the parachain bond reserve. Nevertheless, incentive models where nodes must be compensated through the issuance of tokens rather than transaction fees do hint at a problem with velocity.

2. Microscopic On-chain Stablecoin Footprint

Stablecoins are arguably the most popular application of blockchains so far; they are a facilitator of economic activity and are always in demand by real users (be it for hedging, payments, or just savings). The demand for stablecoins is a proxy for indirect expression of real-world adoption by people; if stablecoin utilization is high, then it is likely coming from a pragmatic stance. Reaching above $120 million USD historically, the dwindling of on-chain stablecoins issued to below $8 million USD shows disregard from major providers, likely hinting out that there are no real users that need stablecoins.

3. Active On-Chain addresses

Coming in at a very uninspiring ~3,300 average daily active user count, the utilization of Moonbeam is astonishingly low for an asset with a market cap of over $150,000,000 USD. Coupled with the pseudonymous nature of blockchain leading people to have multiple accounts, the active addresses do reflect the even smaller reality of true users (a number likely below the difference between average daily new users and average daily users, which is roughly {~2,500} ~3,300 minus ~800).

🧐 Opportunities (External) (Helpful)

1. UniSwap Enters the Chat

Uniswap is the leading DEX protocol. It leads the space in terms of technological standardization, hosts the most liquidity, and has, by far, the largest user base. The presence of Uniswap on Moonbeam unlocks the potential for more transactions to take place and is a vote of confidence from the Uniswap team; if GLMR was going to fail, then odds are Uniswap would not have invested their time pursuing the integration.

2. Microscopic On-chain Stablecoin Footprint Floating roughly around the 7.5 million USD mark, Moonbeam's tiny amount of stablecoins issued presents itself as an opportunity in the event of more stablecoins coming online. Growth of this segment would have explosive positive feedback due to the currently low level. An increase in stablecoins would signal a growth in on-chain users, which would in turn, signal growing demands for GLMR tokens as gas for network operations, which would then feed back into more users that demand stablecoins. Moreover, with the expansion of stablecoins, the reserve collateral on DEFI would likely grow in tandem, providing economic benefits to other projects building on top of GLMR.

😳 Threats (External) (Harmful)

1. Loss of Prominence in DOT ecosystem

Competing in the Polkadot ecosystem requires a very high level of intelligence. The Parachains that are deployed in the DOT ecosystem have heavyweights in terms of the level of quality of the teams. Moonbeam may be the leading chain at the moment, but nothing is ever guaranteed, and in the event that other chains begin to outperform it, a self-cannibalizing effect may take place where developers shift their attention and begin allocating their time to the new rising stars instead. To be fair here as well, abandonment by developers is a threat vector that plagues basically every single blockchain network/project; here, we are specifically referring to abandonment due to a transformation in sentiment around what is more interesting.

Takeaway:

A tech-focused underdog that is leveraging multiple ecosystems.

Positioned to benefit from both breakthroughs in the Ethereum/EVM universe as well as Polkadot, Moonbeam has many desirable characteristics that have garnered strong support from both of the ecosystems.

The lack of any existential threats or crippling weaknesses stands out as a marker of the project's quality.

The contributions of Moonbeam to Polkadot (and all of the projects building on it) with the MRL function that is actually compiled into the programming logic highlight the prominent role that Moonbeam has as being the first parachain to become operation on Polkadot.

Conclusion:

Something that was not covered in the SWOT but deserves at least a mention is Moonbeam's Ignite program, which incentivizes and supports projects that are currently building on GLMR. The initiatives to grow end-user-facing applications are a positive signal for token holders, as ultimately, it is those apps that will drive economic value back into the ecosystem.

Would I invest in Moonbeam?

Yes.

Although I'm not too happy with the token distribution (~70% is in the hands of private groups, the team, and the foundation), it seems as though all three of the parties are intellectually aligned.

The way (IMO, NFA) to make a good play on GLMR is through allocating it to other platforms (liquidity for Stellaswap or lending on Prime Protocol) and leveraging the return potentials. The reasoning behind such an approach is rather simple: with a market cap of ~$150,000,000 USD already, the raw return potential of just HODLing is lower than it would be with a $30 million market cap asset.

If you know something that I don't or feel as though I might have missed anything worth noting, please do share; I would tremendously appreciate some feedback.

Thank you so much for reading.

I hope this serves you well on your journey.

Live long and prosper 🥂