Hype vs. substance

I’m coining the word ‘disruptobloat’ to describe a distinct season that any major technology goes through:

- VC funds are running high for 50 versions of the same use case.

- Everyone’s LinkedIn tagline indicates they’ve been a decade-old expert in [some new tech] (I say this shamelessly, as my own LinkedIn includes both crypto & AI)

- Headlines slowly move from “all companies are building in [tech]” to “Are consumers fed up with [tech]?” to the merciless butt-of-the-joke and “what went wrong”.

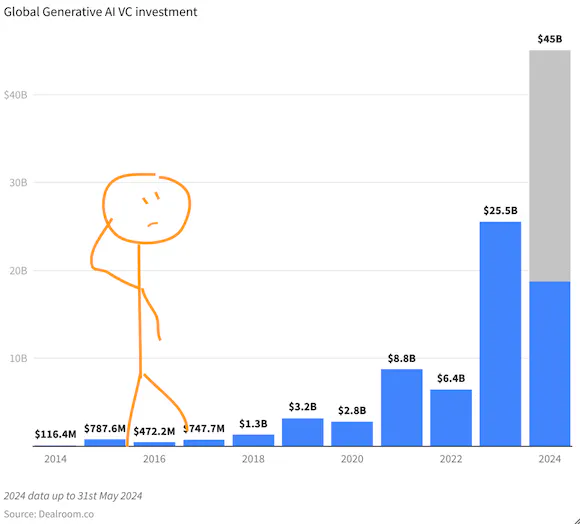

Disruptobloat is a phenomenon of overproduction: [some new tech]-driven products flood the market, diluting the perception of value in the short term.

It’s a race towards the same thing: discovering a sticky use case that shapes new customer behaviors and accrues value. It’s not a bug; it’s a necessary step in the evolution, and a good thing! The bigger the disruptobloat, the faster we get to breakthroughs, because we iterate through ideas faster.

Azeem Azhar from Exponential View breaks it down this way:

Level 1: Do what we do cheaper: (…) automate routine tasks.

Level 2: Do what we do, just do it better: (…) opportunities for qualitative improvements. A major investment bank, for instance, recently used AI to automate much of its unit test coverage. This reduced costs and allowed for more comprehensive testing, improving overall software quality.

Level 3: Do entirely new things. This is where the true potential of AI begins to show (…) But here’s the rub: most businesses are stuck at Level 1 or Level 2. They’re using AI to shave costs or incrementally improve processes, missing the opportunity to strategically rethink what their business could look like (…)

The thing is, everyone is trying to “strategically rethink what their business could look like”, but it’s tough. We’re all conditioned to think through the implicit constraints of our day-to-day lives, and rethinking only happens when we ignore those constraints. For existing businesses, they’re also the constraints of the ossified ecosystems of customers, partners, revenue, and profit.

The Commoditization of AI Models

There’s a saying that originated during the Gold Rush: "When people dig for gold, sell shovels”, used often to describe a business strategy: instead of directly participating in a competitive and speculative market, provide the essential tools and services for that market. The problem with shovels, though, is that they’re fungible, and

Let’s assume that no provider releases a model that is orders of magnitude better than the competition for a long enough time for it to strategically matter__2__. Where does the value accrue, then? In other words, what kinds of products will be able to build a moat?

The application layer__3__ - the surfaces, apps, sites through which users will interact are:

- most likely to shape new behaviors, teaching users to do entirely new things, so

- likely to accrue much more value over time by building new markets

No surprise, then, that it’s worth to compete with hundreds (if not thousands) of startups for the same use cases.

This quote from

- AI tools that run on top of existing software (think: automatic meeting notes for Zoom meetings)

- AI tools that run on top of existing software that have a shot of displacing that existing software (think: meeting notes for Zoom Meetings…where said company then builds video conferencing and pitches you to ditch Zoom)

- AI tools that turn into labor — a net-new category, completely untouched by software until this point (think: the software conducts the meeting for you!)

Hence, disruptobloat.

The Unbundling of GPTs

This race between existing companies and 0→1 startups is a pure Product Discovery Challenge. In theory, model providers should have an advantage, a result of having collected 2 years of usage data. Looking for insight from OpenAI’s marketplace of GPTs returns

It's reminiscent the

Vertical Integrator Strategy

Last week, Not Boring by Packy McCormick published

Vertical Integrators are companies that:

- Integrate multiple cutting-edge-but-proven technologies.

- Develop significant in-house capabilities across their stack.

- Modularize commoditized components while controlling overall system integration.

- Compete directly with incumbents.

- Offer products that are better, faster, or cheaper (often all three).

NVIDIA is an example of this strategy on steroids, building ecosystems around the core technologies to control the entire technology stack, especially as base models become commoditized:

- Hardware (GPUs, A100, H100, DGX, Jetson)

- Software (CUDA, TensorRT)

- Platforms: NVIDIA Omniverse for 3D simulations, NVIDIA Clara for healthcare

- Robotics Lab and Issac Sim robot simulator

- NVIDIA DRIVE for autonomous vehicles, both hardware and software (DRIVE AGX, DRIVE OS).

Not all incumbents are or will be competing in every layer now, but the point is that they have the capability to do so, whether by building or acquisitions. As

“This is the flaw with looking at Square and Stripe and calling them commodity players. They have the distribution. They have the engineering talent. They can build their own TiVo. It doesn’t mean they will, but their success hinges on their own product and engineering prowess, not on an improbable deal with an oligopoly or utility. ”

The Parting Gift

One of the early goals I had for this post was to pinpoint the killer use cases, which, in retrospect, is a tall order for a few hours of research. Still, as the hype slows down, there are a few corners of disruptobloat that I’m paying attention to:

- Lowering the cost of previously highly desired, but high-price services - legal, finance, healthcare - where low cost can create massive demand. From

a16z (again): “LVMH likely spends tens of millions of dollars a year fighting counterfeit goods, sending cease and desist letters, cooperating with law enforcement, etc. How many small Shopify merchants might want the exact same service? All of them! How many could spend $50M/year? None of them. How many might spend $1,000/year? Maybe all of them?” - Democratizing complex skills, like we did with coding. Most of the narrative around the LLM-assisted programming focuses on cost savings, but the magic of it is that it enables people to entirely new things they couldn’t do before. We’ve heard this for a while, first with coding bootcamps, then with no-code apps, but those came with limitations. Now there are none.

- Hyper-personalization at scale, across any consumer activity

- AI + Robotics

- Climate tech__4__

The killer use case is somewhere out there, unrefined and drowning in noise. Whether - or when - the

PS: I post at https://hypegeist.substack.com/ about emerging tech and would love to send these to you directly.

PS2: Thank you Claude for brainstorming and edit assist.