Unlike the mysterious realm of mempools and MEV bots, the world of long-term earning strategies, such as providing liquidity to Uniswap v3, is generally considered relatively straightforward. Publications, research, and expert opinions on Uniswap v3 concentrated liquidity provision abound. But if you dare to look deeper – and if you have the right tools – you can still find all kinds of anonymous sorcerers, strangers, and beasts.

This study started as a part of an ongoing joint research project by teams at Grantfin and Datamint, aimed to develop novel strategies for managing Uniswap v3 liquidity in a high-yield risk-managed way. But when we started analyzing and visualizing liquidity distribution, little did we imagine that we would find and research some truly exceptional players.

We are talking about liquidity providers that make actions so big, so bold, and, in some cases, so crazy that they affect the market in a major way. Yet, almost no one notices them. Why? Because there are a lot of tools that display current liquidity distribution in the protocol (albeit not always correctly, as we highlighted in this article - Here’s Why All Your Uniswap v3 Liquidity Farming Calculations Are Dead Wrong! ), but there are no tools that let you analyze historical liquidity data. If you missed something, it’s gone. And there is no easy way to research the behavior of specific actors.

But we will show you some of these mysterious liquidity providers — and, hopefully, they will help us learn something about Uniswap V3 liquidity provision on Ethereum.

Why researching Uniswap V3 liquidity providers ishard

Upon the realization that all blockchain data is open and public, one's first impression is usually, "yay, I'm an omniscient wizard now!"... but the reality is a bit tougher. Even open data can be so complicated and so huge that it takes enormous effort to draw any insight or conclusions from it. Uniswap V3 is no exception.

Uniswap V3 introduced a novel feature known as concentrated liquidity, a significant evolution from the standard automated market maker (AMM) model used in previous versions. Traditional AMMs spread liquidity across an entire price range, whereas concentrated liquidity allows liquidity providers (LPs) to allocate their funds to specific price ranges. The below image, taken from Uniswap V3’s white paper, displays this concept of concentrated liquidity and how it differs from the traditional AMM.

Graph I represents the V2 model (a traditional AMM), in which liquidity is spread evenly from 0 to ∞. Graph II shows concentrated liquidity: evenly distributed liquidity spread across a set price range (Price A to Price B). Theoretically, you end up with something that looks like Graph III, where liquidity becomes concentrated around the current price.

By allocating to these specific price ranges, LPs have the flexibility to set “custom liquidity bounds,” essentially creating a targeted price window within which their assets can be traded. By doing so, LPs can potentially increase their capital efficiency and earn more trading fees relative to their position size, especially in ranges with high trading volume. This is why, theoretically, you end up with something like Graph III. The majority of LPs will base their price ranges around the current price, with fewer and fewer players having liquidity on the outer limits. This approach, however, also adds complexity and risk, as misjudged ranges could lead to impermanent loss and an underperforming position.

The graph below provides an example of how the liquidity distribution for the USDC-ETH (0.3% fee tier) pool could look on Ethereum at a given moment. As you can see, it is close to the theoretical liquidity provision demonstrated in Graph III of Uniswap’s white paper. In actuality, most of the liquidity does concentrate around the current price, but there are clearly some exceptions.

This is because, when the current price gets out of range and the positions stop earning fees, the liquidity provider faces a tough decision: to rebalance liquidity to a new price range, or to do nothing and hold their position in hopes that the price will come back into their range (reserving the additional option of exiting!). This is a difficult call because rebalancing comes with costs including gas fees, cost of realization of a portfolio loss due to change in asset prices, and swap fees (fixed fees and price impact influence).

Analyzing Uniswap V3 liquidity is similar to analyzing an order book, but with several important differences:

- All liquidity is visible. In traditional order books, most of the liquidity is hidden (even in “lit” pools), meaning that, at any given moment, only a small fraction of market makers’ liquidity is visible in the order book in a form of limit of marketable orders. There is some "hidden liquidity" in Ethereum, though, provided by Just-In-Time (JIT) MEV bots. However, it accounts for less than 2-5% of the market. We will talk more about JIT liquidity later.

- You can identify owners of specific liquidity positions, whereas orders in the traditional order book are anonymous.

- Liquidity providers (market makers) and traders are clearly separated. A market maker is always the AMM pool (that manages the money of liquidity providers), while all users are traders. In most traditional stock markets, you cannot tell which order is placed by the market maker or trader.

These differences create unique opportunities for data analytics if you have the right toolset to overcome the complexity of the blockchain data. There are currently limited options to accomplish this.

As there are no ready-made services to visualize historical data, we have created one ourselves, based on the Datamint Data Engine. Fortunately, the Datamint Data Engine already contains high-quality indexed DeFi data (including all DEX trades and liquidity events), and allows real-time execution of complex analytical SQL queries. That was an absolute requirement for creating liquidity analysis and visualization tool.

Essentially, our service takes all the liquidity events related to a specific poll, and replays them to fill out a liquidity heatmap tick by tick, day by day. Once you see some anomalies, you can query specific positions and explore properties like price range, liquidity, profit and loss in USD (realized or unrealized if the position is not closed yet), and accrued fees. The last of these is the most difficult, as there are no specific logs in Uniswap V3 that detail fee accrual.

The top pool in Uniswap V3 from 2022 to 2023

Let's start with an example by looking at the liquidity heatmap of the top pool in Uniswap V3 over the last year: USDC-ETH (0.05% fee tier).

*Note: we will use the July 2022 - July 2023 timeframe for this and all subsequent heat maps.

We can immediately see how liquidity distribution changes over time. Each pixel of this chart represents liquidity assigned to the specific tick (minimum quantity of the price range) on a specific day. The brighter the pixel is, the more liquidity it contains at that point in time. We can see that concentrated liquidity generally follows the actual price. There are some noticeable patterns; for example, higher expected volatility corresponds to the wider price range used by the majority of liquidity providers. However, the distribution is not uniform and smooth. That's because it is a superposition of many players, some of which are so big that their individual positions appear on the heatmap as bright rectangles.

Vertical rectangles represent wide-range, low-risk, low-yield positions (highlighted by the red oval in the image below), while horizontal narrow lines represent narrow-range, highly concentrated, high-risk positions (highlighted by the yellow oval).

Some positions are so outstanding that we just couldn’t resist researching them in more detail using Datamint’s liquidity analysis tool!

Here follows our ranking of the top 5 mysterious liquidity providers:

5th place: the Blind Shooter

If you look closely at the heatmap above, you can see long horizontal lines that represent the liquidity supplied in a very narrow range. This is a risky bet on the fact that the price will fall into this narrow range and stay there long enough to produce nice revenue from fees before suffering from impermanent loss.

Here is the most interesting example that we found:

Someone has opened an out-of-range position (meaning that the current price was outside the position price range) by supplying over 500K USDC. It happened on the 30th of November 2022 – over 250 days ago at the time of writing – and this position is still open.

Now that looks strange! Why would someone supply half a million dollars to Uniswap V3 for over 8 months for it to simply sit there and earn no fees at all?

Out-of-range liquidity provision is not strange by itself. If you have only one asset out of a pair, and you expect the price to move to some specific price range soon, then you can supply that one asset by choosing an out-of-range position. In this case, you save on swap fees (because you don’t have to swap part of your portfolio to a second asset of the pool), which can be truly beneficial on large orders. What is strange is that, although the price never moved to the price range of that position, it has remained open for this long. So, $500K is just sitting there earning nothing.

The only rationale for this behavior that we can think of is using a narrow Uniswap position as an exotic way to implement a limit order. If and when the USDC/ETH price crosses the price range of this position, the whole USDC amount will be converted to ETH. So, instead of paying a 0.05% transaction fee, our Blind Shooter will receive some fraction of the transaction fees paid by traders for consuming his USDC liquidity. Given the size of his position, that will create a momentary gain of at least 300 USD. That doesn’t look too big, though, considering he currently suffers an impermanent loss of at least 30% due to missing the opportunity to gain from the rise of Ethereum price.

Some concerning thoughts even flashed through our minds, like maybe he placed this order and then something happened to him. We were relieved when we checked his activity and saw that his last transaction was sent just 50 days ago! So, this behavior was intentional… maybe… at least we want to believe…

4th place: the Enigmatic Trader

Next in our research was another major pool: WBTC-ETH (0.3% fee tier). It is special because neither of its two tokens is a stablecoin; rather, they are blue-chip cryptocurrencies. We can immediately see that this pool’s liquidity heatmap is quite different.

Most of the liquidity in this pool is generally supplied into a much wider price range. This is no surprise, because BTC and ETH prices are highly correlated with each other. The most fundamental events in the crypto industry affect them simultaneously. Changes in their relative price are much closer to a random walk or “white noise,” and are thus less predictable for liquidity providers.

So, it looks like liquidity provision strategies are straightforward in this pool: take the average price, choose a wide range (like +/-2 sigma), rebalance rarely, and enjoy. By the way, WBTC/ETH pools are the 2nd and 3rd most profitable pools (aggregated for all providers) in USD, generating around $40M in net profits for their liquidity providers during the last 12 months.

But there are always some whales who like to swim against the current. Just look here:

Somebody has opened another huge out-of-range position by deploying 5,270 Ether liquidity (almost $10M at the time of writing).

Now, this is really strange. At first glance, this position — which, by the way, is still open —is profitable in USD.

Its net value is now $236K higher than at the time of opening. That is ~2% in ~22 days, which is actually very good. The catch is that the relative WBTC/ETH price now is almost the same as at the time of opening this position. That means that if this trader had opened the in-range position (for example, 50% WTBC, 50% ETH), he would have had the same increase in net position value plus he would have accrued a nice amount of fees. So, our estimate is that he just missed an opportunity of earning an additional $5K to $50K (depending on the price range).

So why didn’t he open this position in the money (ITM)? We don’t have many hypotheses for this. The only rational explanation we can see is that this position is part of a complex, carefully hedged strategy. Or maybe we’ve just found a wealthy fan of Ethereum who wanted to create a level of price support for Ethereum relative to Bitcoin?

We will never know for sure. We just want to hope that this is a calculated strategy and not a mistake. Why? Simply because we love data-driven risk-managed investment gains ☺ (don’t you?).

3rd place: Mr. Unlucky

Taking a closer look at the same WBTC-ETH pool liquidity heatmap, we found out that not all major liquidity providers favor wide price ranges. Take a look:

Yes, that is a narrow-range position worth $10M that lasted less than half a day.

It was in the opening range, and there were no signs of trouble. But in just a few hours, disaster struck Mr. Unlucky. The prices of both Ethereum and BTC dropped significantly, which resulted in a $400K+ loss before the position was closed. This is a good example of how investments into correlated asset pools do not protect you from market risks.

Even more heartbreaking for Mr. Unlucky: the prices recovered in less than 10 days. This is also an example of how a stop loss triggering too early can kill your profits. But who are we to judge?

Checking other positions of the same liquidity provider, we can see that, although he earned more than $4M in trading fees over his lifetime, his net loss is over $2.5M.

Well, we all have bad days…

It is also important to note that we analyze the performance of individual Ethereum wallets’ Uniswap V3 operations only. Meaning, it is possible that this wallet represents only a part of a wider, more complex strategy that uses some hedging tools such as call/put options. If this is the case, then the losses we see could be offset by profits from derivatives.

But if that is not the case, please accept our sincere condolences, aavebank.eth (0xD730cd62CDA9cfdc109Be2d819B0337fafdCA959). On to the next one!

2nd place: the Money Mastermind

Ok, it’s time to explore some of the less liquid pools. We don’t want to get too deep in myriads of newborn tokens today, so let’s choose the popular Chainlink pool, LINK/ETH (0.3% fee tier) and jump straight to the heatmap:

What have we here? Well, we see that the total liquidity of the pool increased significantly in Q3 2022. At first, liquidity providers preferred wider ranges, but in Q2–Q3 2023, narrow ranges started to prevail. That usually happens when tokens gain true traction, utility, and adoption, making volatility decline significantly.

We can see that even in 2022, however, there was one brave guy who put his stake into a really tight price range. And you know what? That paid off!

It is clear that the size of this position was massive in comparison to the total value locked (TVL) of the pool. If it were opened today, it would account for more than 1/3 of the total pool size. Opening a position of this relative share in such a narrow price range guarantees that you will take home the majority of fees (provided that you haven’t miscalculated and that the price stays in the range of your position).

In the case of this brave Money Mastermind, it worked perfectly well. The position was open for 7 days, and for a good share of this time it remained in range. More importantly, the position was closed before the LINK price went down.

According to our estimates, this provider earned $500K, including $60K in fees, in just 7 days on a $6M investment. That’s over 9% in a week. Impressive!

1st place: the Wealthy Prophet

Are you ready for a true whale? We have one for you.

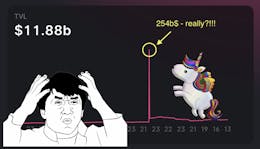

Let’s take a look at a special case of Uniswap V3 pools: a stable pool. We have chosen the USDC-USDT (0.01% fee tier) pool for a detailed analysis. Stable pools are attractive for liquidity providers because the price is virtually constant, so the impermanent loss risk is minimal and you earn anywhere from 1% a year on the low end to 2–3% on the high end from fees alone. Theoretically, one may expect the heatmap of a stable pool to simply look like a straight line of highly concentrated liquidity and tight competition of the major liquidity providers.

Reality is different, though. Most of the time this pool behaved as expected, but when USDC de-pegged for a short period of time earlier this year, things got crazy. So, we decided to thoroughly research what was happening with liquidity around the de-pegging event.

Here is where we see a true whale. On February 9th of 2023, someone added around $75M to the pool in three transactions. Our ability to identify wallet owners in blockchain is limited in most cases, but the contract that handled these liquidity operations is labeled as “1inch Team Investment Fund” on Etherscan.

After 22 days, the position was closed. Its profit and loss (PnL) was positive, which is no surprise, but its size was far from impressive – only $26K (100% from fees). This corresponds to less than 1% annual percentage yield (APY) if annualized. This is probably because Uniswap v3 handles a much smaller USDC-USDT swap volume than Curve, which is specifically designed for swapping stablecoin to stablecoin.

But the truly amazing fact is that this position was removed only 4 days before the shocking USDC de-peg event. Even an actual decline of a 4% USDC price – if realized by stop loss – would have resulted in more than $1M in losses in a day. At that point in time, nobody was sure that the USDC dollar peg would be restored, and potential losses could have skyrocketed. But not for this liquidity provider who earns 1st place on our list and the honorary title of “The Wealthy Prophet!”

Conclusion

That is all for today, but we’ve put together some final thoughts.

This article is in no way financial advice, but it demonstrates the power of a data-driven approach to an empirical analysis of on-chain DeFi operations.

Here are the key takeaways:

- Uniswap v3 liquidity analysis is not an easy task, but if done properly, with the right toolset and competence, it can bring a lot of value to liquidity provision strategy development and analysis.

- Uniswap v3 is a competitive venue. Studying the behavior of big players is a must for the development of a successful LP strategy.

- Liquidity provision is no longer a “set it and forget it” type of strategy. It requires thorough analysis and planning, which, if done properly can yield significant alpha, as shown by the empirical research.

To some extent, this research demonstrates that even big players make mistakes. That creates an opportunity for smaller, but more efficient players; if you want to enter this space, then the sky is the limit. Just don’t expect an easy journey.

So, be ambitious, do your own research, and may the data be with you!

Acknowledgements: We would like to acknowledge the Datamint technology team that provided high-performance access to indexed blockchain data and helped develop the tools for visualization of liquidity heatmaps and for in-depth research of specific liquidity providers and their positions, including the most complex part: calculating the historical dynamics of accrued fees.

Disclaimer: Our calculations may contain errors. In data projects for enterprise clients, we use documented methodology, autotests, and many other tools to achieve the highest data quality. Those tools would be overkill for a short-term research project like this. This research highlights some extreme examples in available data, rather than making assessments and providing curated data for decision-making support.

About the authors:

Ivan Vakhmyanin is a data analytics and visualization (BI, Big Data, Data Science) expert with years of experience. He is also a blockchain and Web 3.0 adept making the on-chain data from leading blockchain platforms (Ethereum, BNB Smart Chain, Solana, etc) available for analysis. Ivan is passionate about sharing experience by developing educational materials and programs in the field of data-driven management for specialists and executives.

Tom Grant is a founder of Grantfin. He previously founded ILA Capital, an investment firm focused on peer to peer lending and exited that in 2021.

Isabela Bagi was an analyst at ILA Capital and co-founded Grantfin in 2022.

Datamint is a value-added blockchain data provider specializing in customized research and development. For more details, visit

Grantfin, a startup focusing on decentralized finance, enables investors and customers to see real-time and historical returns for liquidity pools which support blockchain-based dexes. For more details, visit

Also published here.