426 reads

Consumer Fintech & Crypto currencies: The Twain Shall Meet

by AndreaJuly 15th, 2020

Too Long; Didn't Read

The boundaries between “traditional” consumer fintech companies and cryptocurrency will become even blurrier, as the former can leverage crypto-assets to create new revenue streams. With more transactions moving from cash to mobile phones, companies will have broader target customers of potential crypto services in finance. The application of cryptocurrencies, with relatively lower transaction fees on the blockchain, can empower startups to serve cheaper financial products than the incumbents. For the startups that have already targeted the unbanked/underbanked population, offering crypto-related services can differentiate the product.People Mentioned

Companies Mentioned

1+1>2

Since 2017, thriving innovation in cryptocurrencies and blockchain has formed a strong force that the world can no longer ignore. I believe in the coming years, the boundaries between “traditional” consumer fintech companies and cryptocurrency will become even blurrier, as the former can leverage crypto-assets to create new revenue streams.

With more leading consumer fintech companies and startups expanding services related to crypto-assets or even issuing their utility tokens, the ones that don’t may take the risks of losing a great pie of potential market shares. For crypto-native projects, their participation can create a tipping point for mass adoption.

Positioning cryptocurrency in the consumer fintech space

Let’s give cryptocurrency a new perspective on the industry-level.

Consumer fintech companies are the ones that offer financial services that cater to consumers’ needs, including consumption, investment, borrowing, savings, and transfer that each can be satisfied by a certain type of company.

In the next few articles, I’ll dig into the application of cryptocurrencies in each company type.

Enter crypto in the consumer fintech space (selected companies are mostly in the US/EU/UK)

Why now? The industry backdrop of consumer fintech

Taking a closer look at the recent trend of consumer fintech space, the following points are the ones I think will further incentivize companies to adopt cryptocurrencies.

Cashless payment

COVID-19 has accelerated the trend of cashless payment, especially in regions that previously have lower penetration of digital payment. With more transactions moving from cash to mobile phones, companies will have broader target customers of potential crypto services in finance, which are usually taken place on mobile phones.

Rise of peer-to-peer (P2P) transfer

Recent financial results of leading fintech companies like PayPal, Square, and Western Union show that P2P transfer has shown strong growth. However, the er transfer itself usually doesn’t charge any commission.

Monetization of these customers effectively has become a core strategy for these companies. Offering services related to cryptocurrencies provides an additional way to monetize these users.

Paypal and Zelle have shown strong growth in P2P payment

Serve the unbanked/underbanked

In recent years, startups began capturing the trillion market opportunity of the unbanked and the underbanked, who are usually unqualified for certain or all banking services.

The application of cryptocurrencies, with relatively lower transaction fees on the blockchain, can empower startups to serve cheaper financial products than the incumbents. Coins.ph, a remittance startup targeting overseas workers from the Philippines, converts remittances into cryptocurrencies before being sent to the receivers as fiat.

Also, for the startups that have already targeted the unbanked/underbanked population, offering crypto-related services can differentiate the product and expand the customer base. Revolut, the leading challenger bank based in the UK, has expanded its crypto trading services last month.

Why will more companies integrate crypto in consumer fintech?

In short, cryptocurrency can be the next driver of their revenue.

When new technologies are ready to be implemented, new business models emerge. Just as the cases with AI and big data, consumer fintech companies have integrated cryptocurrencies into their business models.

For leading companies, currently, the customer-facing (2C) business models related to cryptocurrencies mainly include trading or direct selling of cryptocurrencies (ex. Cash App’s buy & sell service of Bitcoin), the extension of existing services integrating crypto-assets (ex. Visa’s recent approval of crypto debit card in EU and UK), and new services for crypto-assets (ex. Fidelity offers crypto custody for both institutional and individual customers).

In addition to these models, existing fintech startups that are smaller in scale than the incumbents have more flexibility of issuing their utility tokens as a way to enhance users’ engagement (ex. Wirex gives you rebate in its tokens after certain consumption with their service).

In the past year, with the popularity of Bitcoin rising, some fintech startups have been planning to integrate both fiat and cryptocurrencies from the start (ex. Plutus allows you to buy brands, including Nike, with up to 3% rebates in its tokens).

As for crypto-native startups, with technological improvement of blockchain and token economics, unconventional business models can emerge such as what we have seen in Decentralized Finance (Defi) projects.

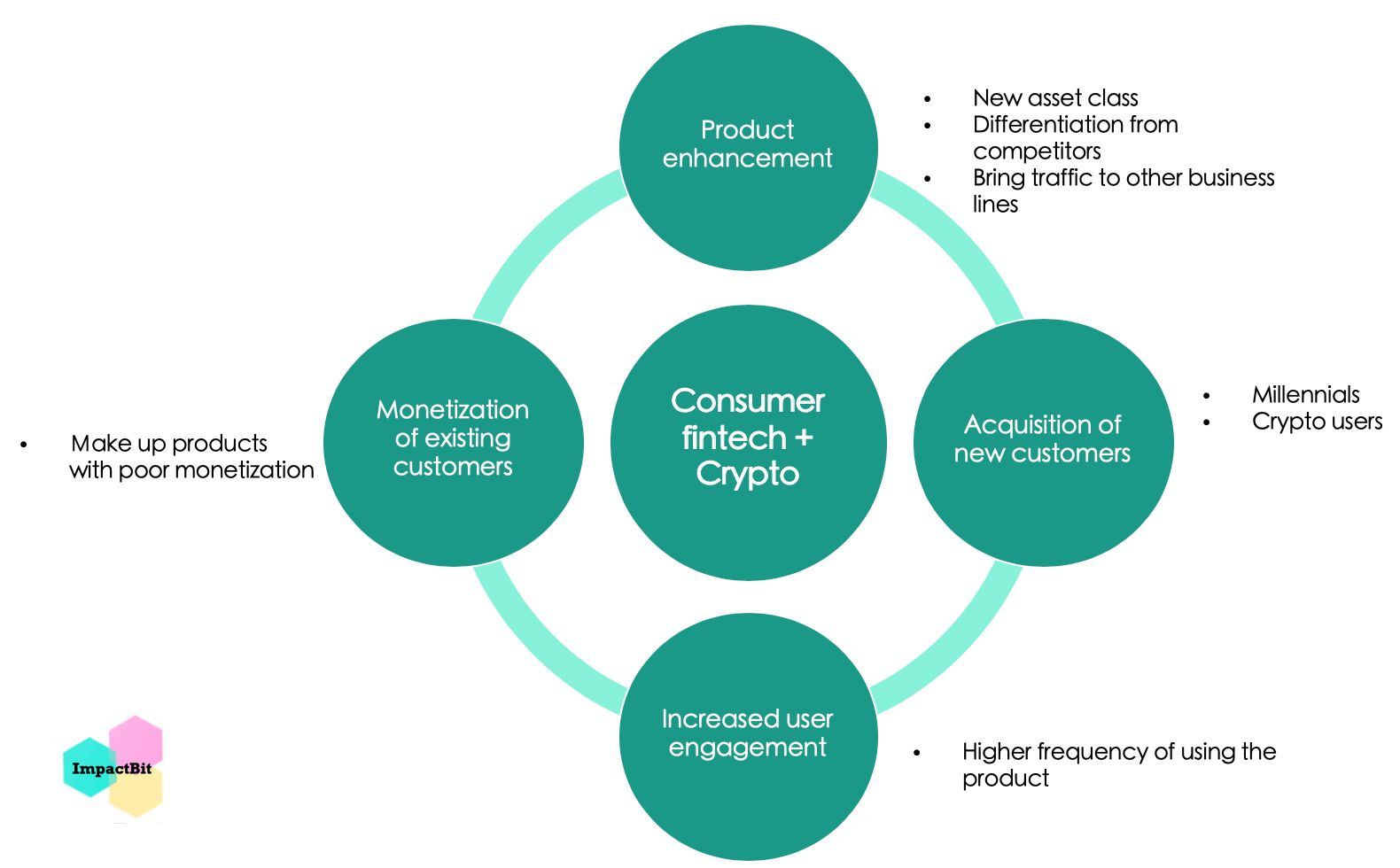

The business model of cryptocurrencies

In my view, with these business models integrating cryptocurrency, companies can achieve revenue growth from these dimensions, including product differentiation/diversification, acquisition of new customer cohorts, increased customer engagement, and monetization of existing customers.

Moreover, with crypto, consumer fintech companies can expand to other types of services effectively like payment to trading.

How crypto can bring revenue growth

The revenue growth effect has already played out. In the latest quarterly financial result, Square’s Cash App reported 306 million dollars from Bitcoin trading, accounting 22% of Cash App’s total revenue, up from 6% in the previous quarter. PayPal’s Venmo, Cash App’s competitor, is also recently reported to begin Bitcoin trading services.

Implications for crypto-native projects

With a larger customer base and lower barrier to entry for mass adoption, I believe the trend of consumer fintech companies integrating cryptocurrencies is extremely positive — for the ones determined to create value. While the crypto community will face more competition from the existing fintech companies, the trend can create higher standards of talents and user experience for crypto-native startups to stand out.

The trend can also attract more capital to the crypto world. Early-stage crypto-native startups will also more likely to become potential targets of acquisition by leading fintech companies. For the ones that are already sitting on piles of cash, mostly crypto exchanges, direct investment/ M&A activities will also become even more active than now (Coinbase, Binance, and Kraken lead in blockchain M&A deals).

While the business models with crypto mostly still revolve around Bitcoin now, I expect regulated stable coins will be integrated into more consumer fintech companies and leading financial institutions in the future, given stable coins’ advantages compared with fiats such as almost-instantaneous transfer, lower commission fees, and 7/24 settlement.

But one thing is for sure — more innovation will come up when the world between fiat and crypto gradually merge into one. After all, innovation knows no boundaries.

L O A D I N G

. . . comments & more!

. . . comments & more!