368 reads

An Internet of Banks; The Future of Defi

by baderOctober 16th, 2022

Too Long; Didn't Read

Ethical hacking is the act of penetrating a computer system or network with the permission of the owner in order to test its security. Ethical hackers are also known as white hat hackers or security researchers. There is some debate over whether ethical hacking is truly legitimate. Some people argue that it is simply a form of hacking, and therefore it is not ethical. Others argue that the hacker has permission from the owner to carry out the attack. There are arguments for both sides of the debate, and it is up to the individual to decide what they believe.Company Mentioned

Coins Mentioned

The Internet of Banks (IoB)

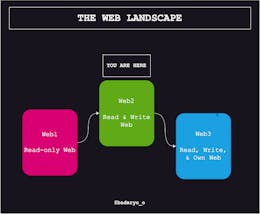

There are numerous terms used to describe the new version of the internet. Most notably, digital money has taken a huge center stage when discussing anything related to technology in the last few years.

Web3, blockchain, DeFi, cryptocurrency, NFTs. All have one thing in common – they define different ways to safely exchange information or money in an interoperable way – or do they?

When Bitcoin originally started in 2009, it had one relatively simple overarching goal - to provide a cashless way to transfer funds without the issue of double spending.

As time passed, more and more blockchains adopted this principle. Before long, we had thousands of cryptocurrencies on the market. Each was powered by its own protocol, technology stack, and community.

This presented a looming issue – People didn’t want to be confined, or locked, to a single currency. They craved interoperability, but more trustless interoperability. After all, the original intent of cryptocurrency was to eliminate any interference when transferring funds.

Each crypto protocol is now behaving more and more like its own self-sovereign, digital bank. Protocols like Polkadot reinforce this concept, as their chain(s) is actually an internet of blockchains that can communicate with one another.

An internet of banks, if you will.

How Substrate Powers the Internet of Banks

Substrate is the blockchain framework that powers the Polkadot network. Essentially, it provides all the foundational parts of a blockchain, which developers can then mix and match modules to create their desired blockchain.

A key part of Substrate, though, is its interoperability. As discussed earlier, this is essential for the growth of the future of web3. Usually, web3 ecosystems abide by a single application or context.

Adoption of web3 will only become widespread if the protocols can communicate with one another in a simple and secure way (especially when it comes to transferring funds).

Substrate’s interoperability is available through its

This segues perfectly into a prime example of how the Internet of Banks is being implemented at this very moment – enter, Sora, which is built on Substrate.

Case Study: Sora

SORA, an on-chain governance system that focuses on DeFi and the Internet of Banks concept, solves a good amount of the problems with interoperability. Their goal is to provide a common protocol that enables users to transact freely in a democratic and scalable way.

Most notably, not only do they implement this within their own ecosystem, but also with other chains in the Polkadot network. Given Substrate’s scalable nature, one could also develop tech to bridge it to other blockchains as well, making it one of the ultimate DeFi solutions.

For example - Sora can be used to create currency that is not just specific to Sora, but to wider applications that don’t even use DeFi. It helps eliminate the usual technical block that most cryptos face. It creates bridges, eliminates the tiresome proprietary of digital ledgers, and encourages growth for web3.

Conclusion

The concept of an interoperable network of payment systems will be a huge part of web3. Any blockchain framework or protocol that encourages and implements this concept will face much more adoption - as users will have ultimate flexibility in choosing how and what currency to utilize depending on the context of the application.

Just as the current internet has many cross-platform formats and methods of communication the future of DeFi will be conducted in much the same way.

The internet of banks is here to stay. It represents a system that has the safety of a traditional bank while giving the user full and secure access to their funds.

IoT, or the Internet of Things, is the propagation of physically gathered data over the internet.

Similar to IoT, IoB (Internet of Banks) represents a more robust and useful version of digital currency. It contains added layers of security, guaranteed uptime, and full control – something which many existing solutions have trouble with.

The face of online banking and finance, as we know it, is about to change forever.

L O A D I N G

. . . comments & more!

. . . comments & more!

About Author

TOPICS

THIS ARTICLE WAS FEATURED IN...

RELATED STORIES

(1/100) Crypto Countdown: Golem #blockchain

Aug 23, 2018